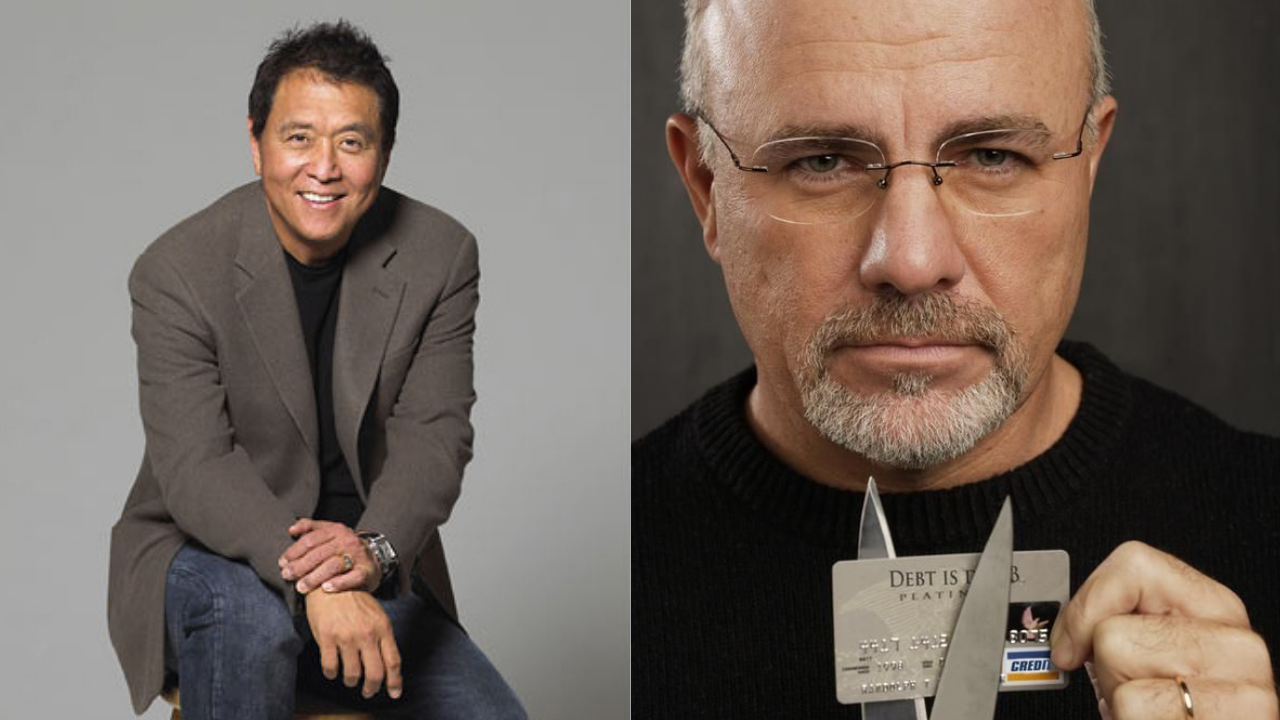

Robert Kiyosaki and Dave Ramsey are probably two of the biggest names in personal finance today. But they have almost polar opposite views on financing and investing. For those not familiar with these two, Robert Kiyosaki is the author of the best-selling book Rich Dad Poor Dad, which he has now turned into a series of books, and a brand of educational games and other media. Dave Ramsey is a best-selling author, a nationally syndicated radio host, and owner of Ramsey Solutions, an educational company that sells personal finance training programs.

Robert Kiyosaki became famous for teaching such unconventional notions as “Your home is not an asset”. Here’s how he defines assets and liabilities, “ An asset is anything that puts money in your pocket every month, and liability is something that takes money out of your pocket every month”. He also believes you should “never say, ‘you cannot afford something’. That is a poor man’s attitude. Instead ask yourself, ‘How can you afford it?’”. These unusual concepts are what made him popular and helped him take the personal finance world by storm. His philosophy on debt is that it should only be used to finance assets like rental properties, not liabilities like cars, boats, and as he says, “doodads”. He believes the key to investing is to leverage your assets to maximize your ability to purchase more assets. Which on some level makes sense because you can grow your investment portfolio much quicker. But this is not without risk!

Kiyosaki Sayings/Philosophies:

- The rich don’t work for money, they have their money work for them.

- It’s okay to make mistakes. (You learn from them)

- Schools don’t teach you about money.

- Financial Education is about debt and taxes.

- Saving money will not make you rich.

- Don’t go to school, get a job, save money, and invest in a diversified portfolio (mutual funds).

- Most poor people confuse liabilities with assets.

- 3 kinds of income: earned, portfolio, and passive.

Dave Ramsey believes in getting out of debt as quickly as possible and never financing anything other than your home. And then, only for 15yrs using a simple fixed interest rate mortgage loan. He also teaches that you should live below your means, use a budget, save for major purchases like a car, and only buy investments with cash. This is obviously a much more conservative approach.

Dave Ramsey is more of a process guy. He uses fewer platitudes and generalizations and offers his “7 Baby Steps” as a step-by-step way to get out of debt and get on a path to wealth. Here are the 7 Baby Steps:

BABY STEP 1

Save $1,000 for your starter emergency fund.

BABY STEP 2

Pay off all debt (except the house) using the debt snowball.

BABY STEP 3

Save 3–6 months of expenses in a fully-funded emergency fund.

BABY STEP 4

Invest 15% of your household income in retirement.

BABY STEP 5

Save for your children’s college fund.

BABY STEP 6

Pay off your home early.

BABY STEP 7

Build wealth and give.

These 7 “baby steps” are part of a larger program Dave Ramsey teaches called Financial Peace University or FPU. FPU is a nine-week course that integrates entertaining videos, class discussions, and small-group activities. The course is designed to teach financial literacy, but its primary goal is to help the participants become debt-free. Dave markets his course and materials mainly to churches and schools. Where they usually buy the materials and have volunteers teach his course. You can find many churches around the country that offer the FPU course. You can also choose to take the course at home as an online self-study course.

What I learned from Dave Ramsey and FPU

Last year during the pandemic our church offered everyone an opportunity to go through Financial Peace University. My wife and I decided to sign up and take the course, as I was interested in seeing what the full course entailed. I have listened to his radio program for years, so I was somewhat familiar with his philosophy and material. Also, I have several friends that have taken the course. All of them highly recommended it. The course was pretty much what I expected. Not surprisingly, it is heavily concentrated on getting out of debt. This part wasn’t very useful to me because we really had little to no debt. We don’t carry a credit card balance and other than a vehicle loan and a mortgage we have no debt. My rental property pays for my truck and my mortgage is at such a low interest I don’t want to pay it off. We only use one credit card for our expenses and pay it off every month. So we’re in pretty good shape as far as debt goes.

While anyone can take the course, it seems to be geared towards couples. Our class was full of couples who were taking it together. This is where I felt the course was really helpful. It showed my wife and I how to get on the same page financially. We have been married for 21 years. In our family, I have always been the one who handles our finances. So, I always know how much we’ve spent each month and all the ins and outs of our finances. My wife, on the other hand, usually had no idea about our finances and really left everything to me. This often led to arguments over our spending. The course did help us learn to communicate better about our finances. I think it helped us realize our financial roles in the family. I'm the saver (fun killer) and she’s the spender (fun maker). This is true for most families, one person is usually the saver and the other a spender. I now understand that she needs to be involved in creating our budget and to have the freedom to allocate some of our money towards spending on vacations and fun things. Now she understands, I’m fine with vacations and fun stuff as long as it is planned, accounted for in the budget, and we stay within our budget.

The FPU course comes with a free 1-year subscription to the premium version of the everydollar.com budgeting app. Using the app to track our spending, helped my wife see how quickly her spending was adding up and allowed her to control it better.

I believe Dave and Robert both have valid points in their messages. That being said, I don’t agree with everything either one of them says. When comes to the use of debt, I kind of fall somewhere in between. I am fairly conservative, so I lean more toward the Dave Ramsey side of having little or no debt. But, I haven’t always felt this way. I used to believe more like Kiyosaki that borrowing money to start a business or buy real estate was a good way to use leverage and get ahead financially. What changed my mind? The 2007 housing crash.

From 2007-2008, during the housing crash, I watched many people who were overly leveraged lose all their investments. At the same time, I knew people who had no debt and cash in the bank. They were the ones who made a fortune during the downturn by buying all the deeply discounted properties. This made me realize debt is definitely a double-edged sword. When used carefully, it could greatly speed up your wealth-building efforts. But, if not used properly it could destroy you financially.

Where I start to slightly disagree with Dave is on using debit cards instead of credit cards. He says you have the exact same protection with a Visa or MasterCard logoed debit card as you do with their credit card. Technically yes, in the event of fraud they will refund or reimburse you for any unauthorized purchases. But in reality, you don’t have the “same” protection because of the difference in the way debit and credit works. Let me explain, when you use a debit card the money has to be in your account for the transaction to be approved and the amount charged is removed immediately. This is not how it works with a credit card. When the amount is charged to the card, as long as you haven’t gone over your credit limit the transaction will be approved. Nothing is taken out of your bank account. Then at the end of your billing cycle, you receive a bill for all the charges accrued during the month. If you pay that bill in full by the due date no interest is charged to the account.

What has happened to me, on more than one occasion, is that I have had charges show up on my account with me still holding my credit card in my wallet. In these situations, I have had to dispute the charges, and once I even had to sign an affidavit swearing the charges are not mine. They were immediately removed and because of the delayed billing, I never paid a penny. If you use a debit card the money comes out instantly, which means any fraudulent charges could also drain your account, and then your card will be declined. It also could cause other payments drawn on your checking account to be declined or returned for non-sufficient funds (NFS). If you do what Dave suggests, which is to cut up all your cards and have only one debit card. You could be in a rough spot if your debit card is compromised and you don’t have any cash or credit cards with you. This could leave you stranded out somewhere trying to buy gas or food. Fraudulent charges are more difficult to straighten out with a debit card because money has to be returned to your account to make you whole again. With a credit card, this situation can be fixed with a simple phone call and no money out of pocket.

Lessons learned from Robert Kiyosaki

The first time I ever heard Robert Kiyosaki was when I came across him on a late-night TV infomercial. He was selling his Rich Dad Poor Dad book. I watched a few minutes and thought he was kind of interesting. Several months later I was in a book store and picked up a copy of his latest book at the time. It was a quick read. It really changed my thinking about some things that I was doing. At the time, I owned a retail computer store. I always thought the key to being wealthy was owning your own business. But what Robert Kiyosaki pointed out was that there are two kinds of business owners. In his book, Cash Flow Quadrant, “S” is for Small business/Self-employed, and “B” is for Big Business. Small business/Self-employed are businesses with few, or no employees other than the owner, or it can be a professional in a private practice like a Doctor or Lawyer. These businesses cannot run without the proprietor. A “B” or Big Business is a business that can run independently of the owner.

Growing up I had friends and relatives who were wealthy and most of them gained their wealth from business ownership. So I equated business ownership with wealth. This is why until I read his book, I thought of myself as a business owner trying to build wealth by starting a business, but in reality, I was really only self-employed. I realized what I really owned, was a job.

I built and repaired computer systems. I had a retail store with set hours that I had to operate within 6 days a week. I wasn’t free to come and go, I was tied to the store. I couldn’t easily expand my business. I would have a hard time finding someone for minimum wage, which is all I could afford to pay someone, that would have the years of experience, skills, or knowledge that I had and the ability to do my job. I couldn’t walk away from my business and have it run without me. Think about a Doctor with his own private practice, he may make a lot of money, but he can’t just hire someone off the street to do his job. If he doesn’t work, he doesn’t make money. Same for me, I couldn’t afford to replace myself with an employee because financially it just didn’t make sense.

Though I find Kiyosaki’s lessons are more inspirational than instructional, I still think there are good thought-provoking ideas in his books. Where I agree with Robert Kiyosaki, is I don’t have a problem using debt to pay for income-producing assets. I have done this myself many times. But I do not believe in being heavily leveraged. Some investors build their portfolio by borrowing money to buy a property, only putting a small amount down, and then use a little cash to fix up the property. After they complete their renovations, they rent the property. Then in a few months, they have it reappraised with the intention of doing a cash-out refinance. This is where they can pull out any equity in the property and use that cash to purchase the next property. Sometimes call the BRRRR Method (Buy, Rehab, Rent, Refinance, Repeat) This works well until you have a market downturn. Because you are moving the equity from the first property onto the next one, you become heavily, if not 100% leveraged in those earlier properties, and in a downturn, this can be a house of cards.

While I have refinanced properties to lower my interest rate and to improve my cash flow by extending the payments out again. I do not cash out my equity. In fact, the last time I refinanced a property was several years ago, and I lowered my interest rate and shortened the loan from a 30-year mortgage to a 15-year mortgage. My payment only went up maybe a hundred dollars. I currently own 19 rental units and all of them are completely paid off. Most of them I have paid cash for and that’s what I prefer, but there have been times when a good deal comes along and all my cash is tied up in other investments. On these occasions, I have used short-term financing to purchase a few properties.

Who is right? Is debt good or bad?

The more I have thought about which one has the better advice when it comes to debt. I have come to the conclusion that it depends on your level of financial education and maturity. If you have little to no financial education then I would recommend that you start with Dave Ramsey. People who are not financially educated often don’t understand how money works. They typically don’t do well managing their finances and tend to get in trouble with credit cards and consumer debt. If you are one of these people or if you are young and just starting out, Dave Ramsey teaches you how to budget, how to get out of debt, and how to stay out of debt. These are good things to know. Budgeting your money and having no debt allows you to save money. Money that can be used to purchase property for cash or used as a down payment on that property. You really should understand the basics of finances, like budgeting and saving money before you begin investing.

If you have little or no bad (consumer) debt and consider yourself to be more financially savvy, you may want to follow Kiyosaki’s philosophy of using good debt to finance income-producing assets. This requires you have the knowledge of how to properly use debt and to have disciplined control of your finances and spending. Using leverage can definitely speed up the wealth-building process but it comes with more risk. Just be careful and don’t get overleveraged!

I think both these men have taught me some important financial and business lessons. While each has his own perspective on financial matters, it is good to hear both sides. I don’t agree with everything they teach but there is useful information to glean from both of them. I recommend reading their books and following them on social media.